Abstract

Newly created cryptocurrency tokens dilute the holdings of existing token owners. If block rewards are taxable income at their fair market value at the time acquired, token holders’ income will be overstated. This report explains dilution and, using the example of a real-life token holder who helped maintain the Tezos cryptocurrency network throughout 2019, quantifies the potential for overtaxation. We show that there is no simple way to adjust the value of block rewards in order to include only true economic gain in taxable income. Our findings support the taxation of block rewards at the time of their disposition, not acquisition, which is the tax treatment accorded to other newly created property.

Article Citation

Mattia Landoni, Abraham Sutherland, "Dilution and its discontents: Quantifying the overtaxation of block rewards 1.0," August 2020.

Table of Contents

The novelty and complexity of cryptocurrency presents challenges for regulators. In tax, the consequences of bad policy would be serious: If block rewards are taxable income at their fair market value at the time acquired, token holders will be taxed on an exaggerated statement of their economic gain. This problem exists both for proof-of-stake (since one must be a token holder to obtain block rewards) and proof-of-work (since in practice many miners are also token holders). And, the overtaxation would be significant — in the real-life example discussed below, taxable income from block rewards would be several hundred percent higher than the taxpayer’s true economic gain. In other realistic cases, the IRS would see taxable income, even though token holders would not have any true economic gain.

This overview of the problem is adapted from an article recently published in Tax Notes.1 The article explains and quantifies the potential for overtaxation for a real-world taxpayer holding cryptocurrency tokens. Here, we present the basic issues and consequences; we refer readers to the Tax Notes article for a more complete explanation of the concepts and models we summarize below.

Dilution is the loss experienced by incumbent owners upon the creation of new ownership units (such as shares or cryptocurrency tokens). When additions to one’s balance from newly created tokens are viewed as an income realization event, whereas dilution is not, net income is systematically overstated. The resulting overtaxation could be a problem for users and block-creators of all cryptocurrencies, and is especially serious for proof-of-stake cryptocurrencies, which rely on token creation by incumbent owners — that is, by token holders — as an integral part of network maintenance.

It’s possible to adjust the value of block rewards to reflect a taxpayer’s true economic gain — this is what we show below — but there is a problem. First, it’s complicated. And second, there is no single correct way to do it. These findings support a policy of taxing block rewards at the time of such tokens’ sale rather than when they are first generated by the block creator.

We define overtaxation as the excess of taxable income under a strict realization approach over true economic income. Our example taxpayer is a Tezos staker — a token holder who acquires new Tezos cryptocurrency tokens by participating in the maintenance of the Tezos network. We present the pros and cons of different methods of accounting for dilution when the cryptocurrency’s aggregate network value, the taxpayer’s ownership balance, and the rate at which dilution happens are all time-varying. We conclude that the acquisition of those tokens should not be an income realization event, although any of the methods we propose would be preferable to an approach of strict realization that ignores dilution entirely. Tax policy aside, the methods we develop to quantify the economic value lost to dilution are independently interesting to investors and other finance and accounting practitioners.

I. Definition of Income

The total change in wealth caused by ownership of an asset is:

ΔWealth = Distributions + Capital Appreciation (1)

where capital appreciation is defined as the change in the asset’s value and can be positive or negative.

Different operational definitions of income imply that different components of the change in wealth are included in current income and therefore subject to the income tax. Under the most comprehensive definition, known as Haig-Simons income, both components are included. Under a “strict realization” principle, income includes distributions only, for the rest will be realized if and when the asset share is sold.

The U.S. income tax is not based on a strict realization principle, however, and taxpayers are often allowed to deduct reductions in the value of their investments (with a corresponding reduction in the tax basis) when these are reasonably certain to have happened and are easy to quantify. The most obvious example is depreciation. If a business buys a car, it does not have to wait until the car is sold to a scrap yard to recognize an expense.

A less obvious example of a reduction in value is dilution. When owning a share of an asset, the capital appreciation is split into two components: the change in the value of the whole asset (prorated by the taxpayer’s initial share), and dilution, defined as the current asset value times the change in the fraction owned that occurs because of the creation of additional shares independent of the taxpayer’s purchases and sales:

ΔWealth = Distributions + Change in Asset Value – Dilution (2)

Like depreciation, in many cases dilution results in an immediate explicit or implicit deduction for the taxpayer. Unlike depreciation, however, dilution is not a formally recognized taxable event and its treatment is determined on a case-by-case basis. For instance, for stock compensation, the corporation receives an offsetting deduction that indirectly benefits the shareholders being diluted. For a pro rata stock dividend, the distribution is not income because it is automatically and exactly offset by dilution.

Cryptocurrencies consist of a number of tokens in a network. If one accepts the uncontroversial premise that the value of a cryptocurrency network does not depend on the exact number of tokens it contains, then the creation of new cryptocurrency units results in dilution. Unlike random fluctuations in network value, which can give rise to both capital gains and losses, this dilution is sure to happen and sure to be detrimental to the taxpayer’s wealth.2

As noted, dilution is fully and automatically accounted for under a Haig-Simons conception of income. Alternatively, dilution need not be accounted for if the acquisition of newly created tokens is not a realization event, as the combined effect will be accounted for at the time of the tokens’ sale. This is the position taken by one of us in a separate article: new reward tokens are created by those who maintain cryptocurrency networks, and taxpayer-created property is not income under U.S. tax law.3 Under this approach, the true economic gains from both newly created tokens and purchased tokens will be accurately established, and can be taxed, at the time of those tokens’ sale. In this report, we focus exclusively on the economic consequences of tax policy.

If new tokens are viewed as distributions — despite the fact they are not distributed by anyone — and are taxed in the year in which they are acquired, current law does not provide a way for the taxpayer being diluted by those tokens to obtain a corresponding deduction.

In what follows we demonstrate that there is no one perfect method to account for this dilution. Accordingly, we propose three candidate methods, each with its own strengths and weaknesses. We then compare the results with an option for the tax treatment of block rewards that would disregard dilution. In 2014, IRS guidance stated that “mined” cryptocurrency tokens (such as bitcoins) are gross income at the tokens’ fair market value on the date received.4 This is a policy of strict realization because it fails to account for dilution. We call this policy of strict realization the cash value approach.

Our comparison is based on a specific cryptocurrency, Tezos. Dilution explains why the cash value approach systematically overstates taxpayer gain and is not desirable as a matter of tax policy. Our proposals therefore provide options for accounting for dilution, to make a realization-based annual tax fair. Each option results from a different but defensible approach to quantifying the economic value lost to dilution.

Because no one option is clearly superior, and because of the accounting complexity introduced by each option, our results buttress arguments against a policy of annual taxation of reward tokens.5

The lack of an obviously dominant option also implies that our discussion is independently interesting to investors in any assets subject to dilution. The accounting methods we develop suggest ways of decomposing investment returns into appreciation and dilution, and to produce consistent financial reporting of business income from cryptocurrency holdings.

II. Accounting for New Tokens

The aforementioned article presents a simple model for establishing true gains and losses from proof-of-stake cryptocurrency block rewards in light of dilution.6 That model is based on two key variables which illustrate the consequences of ignoring dilution. The first is the rate at which new tokens are added to the network: the token creation rate. The second is the percentage of the total supply of tokens that participate in network maintenance through staking: the staking rate.7 The model also excludes any changes in asset value, defined as the aggregate value of all tokens in the network. Later, we begin with this simplified model but then elaborate it to account for the real-world complications introduced when three parameters, held static in the simple model, are relaxed to account for their variance over time.

Tezos block rewards are the result of “staking” one’s tokens (either directly, or through delegation), and staking is required to maintain the Tezos network. Tezos tokens have a readily verifiable market value and, as noted, one option, the cash value approach, is to include reward tokens in gross income at their fair market value in dollars on the date acquired. Tezos tokens are property for tax purposes while taxes must be paid in dollars, and dollars are also the unit of account for most accounting purposes.

Tezos token holders are eligible to create new reward tokens proportionate to their holding, that is, to their ownership share in the network. If all token holders stake their tokens and receive pro rata block rewards, everyone’s share would remain constant because block rewards would exactly make up for dilution. Then it would make sense to treat block rewards like pro rata stock dividends and exclude them from income. In this simplest case, when the staking rate is 100 percent, the token creation rate doesn’t matter. Whether each holder’s token balance increases by 10 percent or 1,000 percent, none experiences any gain and there should not be any income subjected to tax.

If some token holders do not participate in staking and therefore do not receive block rewards, then these “non-stakers” will see their share in the network decrease. If we know the token creation rate, then we know the effect of dilution on those who do not stake their tokens. The dilution rate is found from the reciprocal of the rate of increase of tokens in circulation. If the total supply of a cryptocurrency’s tokens increases by 50 percent over the course of a tax year, every non-staker will see his share in that supply decrease by one third; if the creation rate is 10 percent, the dilution is 9.09 percent.8

The token creation rate is not enough, however, to establish stakers’ gains from staking. Gains — both nominal and real — depend on the staking rate. Dilution affects stakers and non-stakers equally, but the extent to which stakers offset dilution through new tokens depends on how many stakers share in those tokens.9

We can use numbers drawn from Tezos to illustrate this simple model. In 2019 the total supply of Tezos tokens increased by about 5 percent, and so non-stakers’ dilution was approximately 4.8 percent.10 The staking rate varied over the course of the year, but averaged roughly 70 percent. Because the new tokens are divided among stakers, using these rough figures a Tezos staker would end the year with 0.05/0.7 = 7.14 percent more tokens. Accounting for the 5 percent new tokens, however, the true economic gain would be just (1 + 0.0714)/(1 + 0.05) = 2.04 percent.

This simple model is adequate to explain why the cash value approach overstates gain from staking. Under the cash value approach, the tax authorities treat the 7.14 percent new tokens as income, overstating the true gain by 250 percent.

Among other shortcomings, this model does not address the dollar value of Tezos tokens. There is no reason to suppose that the value of a single token, expressed in dollars, will remain constant as new tokens are added to the supply. Otherwise, a cryptocurrency would be a rather remarkable wealth creation machine. If a 10 percent token creation rate is good, 20 percent would be better — so why not 200 percent?

The more reasonable assumption for a basic model is that the total network value remains constant, so that income is a function of distributions and dilution but not changes in asset value. This was the approach taken in “Taxation of Block Rewards.” Assuming the value of the Tezos network holds constant, with 5 percent more tokens, at the end of the year the dollar value of a single token will be 95.24 percent what it was to start the year. With a 70 percent staking rate, a 5 percent token creation rate, and a constant network value, under the cash value approach suggested by the 2014 IRS guidance stakers will show income of 6.97 percent of their initial share in the network.11

In real life, nothing remains constant. First, the value of the network expressed in dollars fluctuates — sometimes wildly. Second, the staking rate varies over time; in 2019 the Tezos staking rate ranged between about 62 percent and 77 percent. (Note that, for a token holder who participates in staking, a higher number means less economic gain). Moreover, in practice reward tokens are not received in strict proportion to the tokens staked, especially over shorter periods of time.12 Finally, stakers’ balances change over time, as tokens are purchased or sold and as reward tokens are added to the balance.

Accordingly, a method of accounting for dilution must account for these three complications:

- the taxpayer’s balance is time-varying;

- the rate of dilution is time-varying; and

- the value of the network is time-varying.

The first complication is just a matter of using the appropriate accounting technique, and the second complication can be dealt with by using the measured rate of dilution. The third complication is the challenging one, because there is not one correct way of handling it.

We can think of at least three defensible methods to account for dilution. We call these the depletion method, the market value method, and the implied dilution method. None is philosophically superior in terms of being “closer” to the concept of “true” economic income, but the methods require different inputs and therefore have different strengths and weaknesses.

Suppose on January 1 the total supply of Tezos tokens was 10,000, and a taxpayer buys 600 tokens at a price of $0.42 per token (or $252 total). Next, suppose that on December 31 the total supply of Tezos tokens rose to 15,000 and the token price rose to $0.50. What is the cost of the dilution sustained by the taxpayer?

A. Method 1: Depletion

While on January 1 the taxpayer owned 600/10,000 = 6 percent of the total cryptocurrency network, on December 31 she owns 600/15,000 = 4 percent, or one-third less. For this reason, the taxpayer takes a depletion charge equal to one-third of the tax basis of her investment, or

![]()

The advantage of this method is that it does not require a market price and it is instead entirely based on transactions that happened in the past. The only data requirement is the total number of tokens outstanding at two points in time. Moreover, it is consistent: The depletion deduction is guaranteed to be less than the tax basis. Because of this consistency property, this method is suited for financial reporting to shareholders by a business that owns tokens.13 Disregarding dilution altogether, as in the cash value method, would result in overstated business income, potentially distorting management compensation or shareholder perception of value. On the other hand, accounting for dilution using an inconsistent method could result in the business holding the tokens at negative book value, also an undesirable result.

B. Method 2: Market-Based

The market capitalization of Tezos went from $4,200 ($0.42 x 10,000) to $7,500 ($0.50 x 15,000), a 79 percent increase in network value, while the taxpayer’s position went from $252 to $300 (a 19 percent return). The difference in return (79 percent – 19 percent = 60 percent of $252, or $150) must be mathematically caused by dilution. Equivalently, if the taxpayer had owned 6 percent of all Tezos in circulation on December 31, her position would have been worth $450 (6 percent x 15,000 x $0.50). Because her position is only worth $300, the value lost to dilution is $150 ($450 – $300).

This method is more complex, as it requires additional information: the price of Tezos at two points in time, in addition to the number of tokens outstanding. The main advantage of this method is that it is accurate: Unlike the depletion method, this definition captures the true economic cost of dilution under FMV (or Haig-Simons) accounting, that is, the third term in equation (2). For this reason, this method is suited for any business purposes that require measuring the true economic cost of dilution, such as performance attribution in an investment portfolio.

Unlike the depletion method, moreover, this method is not consistent. In the extreme, if on December 31 the price of Tezos rises to $1 (twice the previously assumed value), the value lost to dilution is $300 (2 x $150), more than the original cost basis of $252, resulting in negative book value. This problem happens precisely because this method allows the taxpayer to deduct the full market value cost of dilution without requiring her to first realize the market value of her unrealized capital gains — that is, it uses the Haig-Simons approach on the “minus” side but not on the “plus” side.

A less obvious consequence of this inconsistency is that the greater the unrealized capital gain, the greater the taxpayer’s deduction is! Thus, a higher Haig-Simons income (a larger increase in market value of wealth) results in a lower taxable income. For this reason, this method would likely be deemed too favorable to the taxpayer and thus unacceptable as a method of determining taxable income.

C. Method 3: Imputed Dilution

The prior two methods highlight an apparently unsolvable trade-off between consistency and accuracy. On one hand, the market value of rewards is counted as current income, and thus it seems appropriate to offset it using the market-value cost of dilution. On the other hand, the market-value cost of dilution can be greater than the combined value of income from rewards and the taxpayer’s basis in the original tokens. Accounting for tokens at FMV (that is, setting taxable income equal to Haig-Simons income) solves the trade-off but creates well-known problems, which is why the taxation of unrealized gains and losses on an FMV basis has found very limited application in real-world tax systems.14

A potential solution to this conundrum is to directly adjust rewards for an imputed cost of dilution. In our example, the total supply of tokens grows in a year by 50 percent (from 10,000 to 15,000). Our taxpayer begins the year with 600 tokens and would have to acquire 300 additional tokens to maintain her proportionate share in the network. In practice, however, she may receive more than 300 tokens if other token holders choose not to participate in staking. For instance, suppose that 75 percent of tokens participate in staking (that is, the staking rate is 75 percent). In that case, our taxpayer should expect to receive 5,000 * 600/(10,000 * 0.75) = 400 tokens. Of these, 300 (75 percent of all tokens received) compensate the taxpayer for dilution, and the remaining 100 (25 percent) constitute a transfer from non-stakers to stakers, that is, income.

While the explanation is somewhat complicated, the resulting math is very simple. Under this proposal, taxable income is calculated as:

Taxable Income = FMV of Tokens Acquired · (1 – Staking Rate). (4)

This method has two main advantages, both deriving from the fact that it does not affect the tax basis of, nor does it require any knowledge of, existing tokens, and income is defined at the level of individual reward transactions. First, this method greatly simplifies accounting in comparison to the previous two methods. Second, while it is an approximate method, it does come close to solving the apparently unsolvable trade-off between accuracy and consistency, as it roughly captures only the realized portion of the FMV cost of dilution.

This resolution, however, comes at the cost of generality because it embeds knowledge specific to the Tezos network. This is a high cost: While the concept of staking rate exists in some form for most proof-of-stake cryptocurrencies (that is, those cryptocurrencies for which network maintenance is performed by token owners, and thus dilution accounting is most relevant), the rule proposed here is not guaranteed to be easily applicable to every existing and future cryptocurrency. Thus, the greater simplicity in accounting is offset by a greater complexity in regulation — namely, the potential for having as many distinct practical implementations of this method as there are cryptocurrencies.15

Also, the loss of generality is with respect to the taxpayer’s behavior as well. The imputed dilution method essentially assumes that the taxpayer engages in staking directly and without pause throughout the entire tax reporting period. A taxpayer who stakes intermittently or delegates to others could plausibly earn less than necessary to keep up with the creation of new tokens. For this taxpayer, the true net income from holding Tezos is negative, but taxable income is positive. This happens because the taxpayer only gets an allowance for dilution when staking but gets diluted all the time.

III. Real-World Example

Here, we compute the total taxable income of a real taxpayer. Using the taxpayer’s record of block rewards, as well as his purchases and sales of Tezos tokens over the course of 2019, we apply each of the methods just introduced, allowing us to compare the results.

We use four methods:16

- The “cash value method” (include rewards in gross income at their FMV on the date received, with no deductions for dilution, as suggested by the 2014 IRS guidance).

- The “market value method” (dilution allowance based on market value of dilution loss).

- The “depletion method” (dilution allowance based on fraction of initial investment).

- The “imputed dilution method” (taxable income is computed already net of dilution allowance as the portion of reward tokens’ FMV that exceeds the rewards expected in a 100 percent staking scenario).

This taxpayer staked his Tezos tokens throughout 2019, initially by delegating them to others, and later by delegating them to himself and directly operating a computer running the Tezos software that validated transactions. His initial balance on January 1, 2019, was 102,708 tokens. On a number of occasions during the year, he added to his staking balance through purchases of tokens. These purchases totaled 98,554 tokens. On two occasions he reduced his staking balance, selling a total of 460 tokens. During 2019 the taxpayer acquired 8,876 tokens as a result of staking; these tokens were added to his balance on more than 100 different days. His token balance at the close of 2019 was 209,678.

The total supply of Tezos tokens on January 1, 2019, was 781,346,794. During 2019, the supply increased by 39,529,621 tokens or 5.06 percent,17 and at the end of the year the total supply was 820,876,415. The market price of a single token began the year at $0.49 and trended upward, ending the year at $1.32, an increase of 169 percent. The value of the total token supply started the year at $356,735,257 and ended the year at $1,085,198,621, an increase of 182 percent.

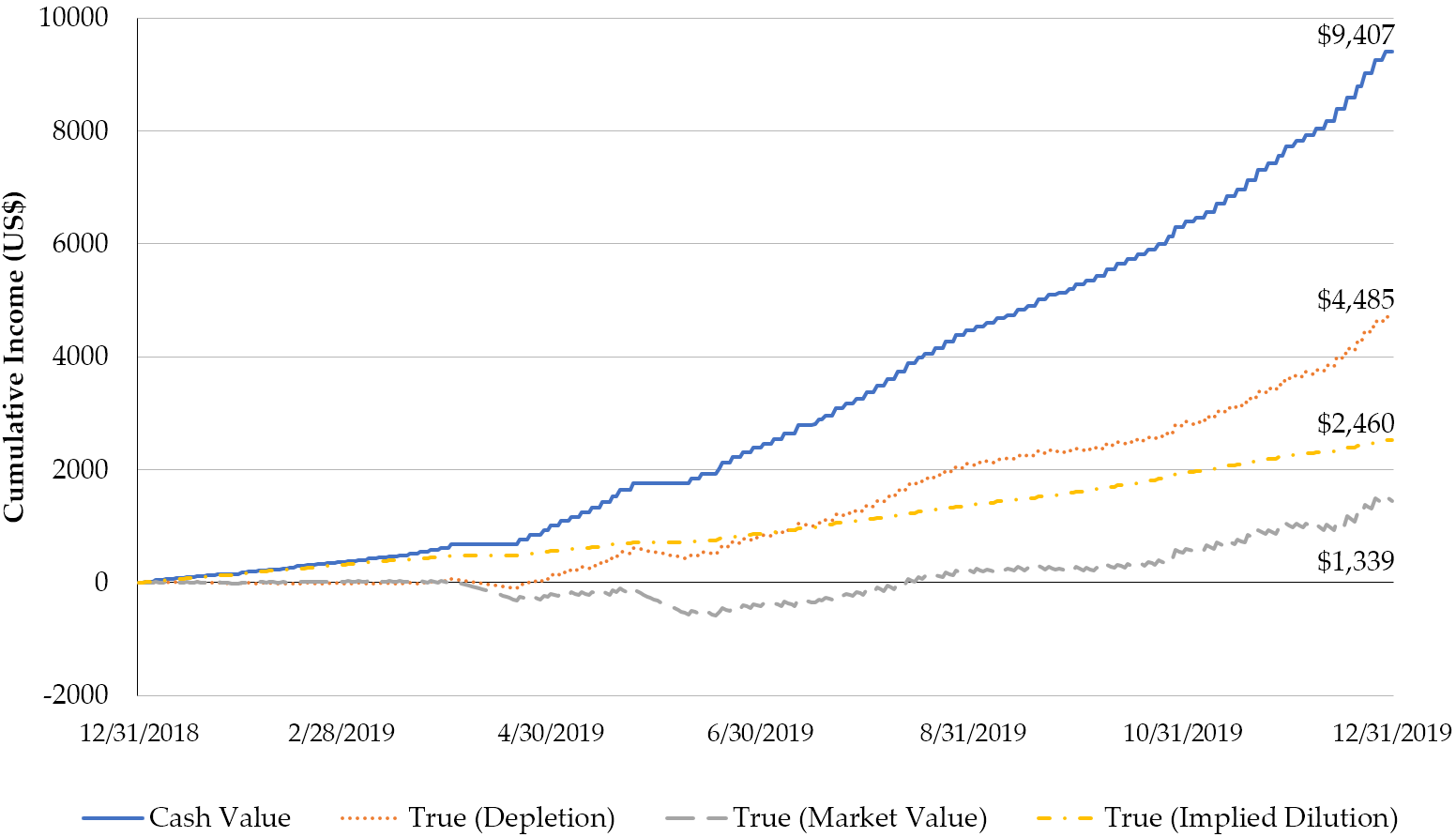

The taxpayer’s 8,876 reward tokens, after adjusting for reward tokens as well as deposits and withdrawals over the course of the year, reflect an annual increase in tokens caused by staking of 5.74 percent.18 The taxpayer reported the gains from his reward tokens by establishing their fair market value on the date they became spendable. On this cash value method, the taxpayer’s participation in the maintenance of the Tezos network resulted in taxable gross income of $9,407. As shown by the chart below, the cash value method greatly overstates the taxpayer’s true economic gain, but each of the three methods results in a different figure for the taxpayer’s true gain.19

Although the outcomes are very different, under any definition of true economic income the cash value approach drawn from the 2014 IRS guidance results in a substantial overstatement of taxpayer income and results in overtaxation.

IV. Conclusion

The creation of new tokens (“block rewards”) is often used as a device to encourage network maintenance and always results in dilution. Quantifying the economic effect of dilution is important for proof-of-stake cryptocurrencies in particular, as their networks are maintained by token owners as opposed to third-party miners. With a cryptocurrency such as Tezos, to participate in network maintenance and obtain block rewards, one must suffer dilution as well. If block rewards are taxed as realized income, without a way to quantify the effect of dilution, cryptocurrency owners will suffer from overtaxation.

In this report we have tried to quantify this potential for overtaxation, illustrated by a real-world taxpayer who held Tezos tokens throughout 2019 and declared $9,407 of taxable income using the cash value method suggested by IRS guidance issued in 2014.

Our methods attempt to reconcile the underlying economics of block rewards and dilution with a realization-based income tax. This turns out to be a formidable challenge. The depletion method is consistent — that is, it never results in a depletion allowance greater than the cryptocurrency’s initial cost basis — but inaccurate, as it does not measure the true market value cost of dilution, whereas income from rewards is equal to their market value. Next, the market-based method is accurate but inconsistent. Finally, the imputed dilution method is simple and offers a practical compromise between accuracy and consistency, but at the cost of generality — that is, it only works under specific assumptions. We estimate that this taxpayer’s true income was between $1,339 and $4,485 — using, respectively, the market value method and the depletion method — resulting in an overstatement of true income of roughly 100 to 600 percent.

Instead of choosing among these methods of allowing taxpayers to realize the value of their dilution, it is simpler and fairer to allow them not to realize the value of their block rewards until they are sold. Recently, some members of Congress have expressed a similar view in a letter to the IRS, writing that block rewards should not be taxed when generated, “similar to all other forms of taxpayer-created (or taxpayer-discovered) property — such as crops, minerals, livestock, artworks, [etc.].”

Aside from tax, the methods introduced here can be useful for valuation and management of cryptocurrency portfolios and inventories. The depletion method is suitable for reporting under delegated management, when realization matters and consistency matters more than correctness. The market-value method is likely more useful for cryptocurrency valuation and portfolio management, when total income (realized plus unrealized) matters. While in that context FMV accounting is both easy and best, our method is still useful to decompose investment performance into rewards, dilution, and actual asset appreciation.

Notes

- Mattia Landoni and Abraham Sutherland, “Dilution and True Economic Gain From Cryptocurrency Block Rewards,” 168 Tax Notes 1213 (Aug. 17, 2020), also available at ssrn.com/abstract=3672461. ↩

- The best analogy is perhaps with buildings, for which depreciation is allowed, even though over time buildings experience both certain physical depreciation and uncertain financial appreciation with uncertain net effect. In this regard, the increase in a cryptocurrency’s network value is highly uncertain: Mattia Landoni and Gina C. Pieters, “Taxing Blockchain Forks,” 3(2) Stan. J. Blockchain L. Pol’y 197-227 (2020), showing that most newly launched cryptocurrencies experience large declines in market price and ultimately fade away. ↩

- Abraham Sutherland, “Cryptocurrency Economics and the Taxation of Block Rewards,” Tax Notes Federal, Nov. 4, 2019, p. 749; and Sutherland, “Cryptocurrency Economics and the Taxation of Block Rewards, Part 2,” Tax Notes Federal, Nov. 11, 2019, p. 953 (hereinafter “Taxation of Block Rewards”) (also available at www.ssrn.com/abstract=3466796). ↩

- Notice 2014-21, 2014-16 IRB 938, Q-8. ↩

- As noted, this report does not address the law that would determine the proper taxation of block rewards. For the argument that the acquisition of block rewards is not a taxable event under the Internal Revenue Code, see “Taxation of Block Rewards,” supra note 3. ↩

- “Taxation of Block Rewards,” supra note 3, at 760-771. The article also presents an overview of how a public cryptocurrency works, at 753-755, and a detailed explanation of how Tezos works, at 755-759. ↩

- In “Taxation of Block Rewards,” supra note 3, the term “validation participation rate” is used to describe what is here called simply “staking rate.” Validation is another common term for what is here referred to as staking. ↩

- (1 – (1/1.5)) = 33.33 percent; (1 – (1/1.1)) = 9.09 percent; see “Taxation of Block Rewards,” supra note 3, at 764. ↩

- Non-stakers’ losses to dilution are equal to stakers’ total net gains from staking. For this reason, stakers’ gains can be viewed as a redistribution from non-stakers. See “Taxation of Block Rewards,” supra note 2, at 764-765. ↩

- Namely, the number of tokens increased from 781,346,794 to 820,876,415, a 5.06 percent increase. For a token holder who maintained a constant number of tokens throughout this period, this results in a 4.82 percent (= 1 – 1/(1.0506)) decrease in the share of total tokens. ↩

- (0.05 * ((1 + (1/(0.05 + 1)))/2))/0.7 = 0.0697. See “Taxation of Block Rewards,” supra note 3, at 766-767. ↩

- In Tezos, for example, opportunities to validate blocks are assigned at random; opportunities to create or endorse blocks can be missed; and delegators may agree to share a portion of their apportionment with those — the delegates, known as “bakers” in Tezos — who operate the computer hardware and software that convert staked tokens into a stream of newly created tokens. For a detailed explanation of how Tezos works, see “Taxation of Block Rewards,” supra note 3, at 755-758. ↩

- To the best of our understanding, the recommended treatment of block rewards under current U.S. generally accepted accounting principles closely resembles the cash-value approach to taxation. The Association of International CPAs considers tokens “intangible assets with indefinite life” (“Accounting for and Auditing of Digital Assets” (2019)). Under this treatment, rewards would be included in net income at market value whereas unrealized gains and losses, including those caused by dilution, would not be recorded. If, instead, the business were allowed to hold the tokens as “trading” securities (see, e.g., Financial Accounting Standards Board, topic 320), it could then use FMV accounting (essentially, the Haig-Simons definition of income) and our argument would not apply. ↩

- The only instance the authors are aware of is Italy’s short-lived experiment in the late 1990s. For an account, see Julian Alworth, Giampaolo Arachi, and Rony Hamaui, “What’s Come to Perfection Perishes: Adjusting Capital Gains Taxation in Italy,” 56(1) Nat’l Tax J. 197-219 (2003). ↩

- In Tezos, for example, the staking rate that determines a staker’s potential to create new tokens is determined at t1, tokens are created at t2, and they remain subject to forfeiture until they are released to the full control of the staker at t3. By design, the elapsed time between t1 and t3 varies randomly between approximately 31 and 35 days. For ease of accounting, our imputed dilution method uses the staking rate as of the date the new tokens are actually acquired. A more accurate method tailored to Tezos would use the staking rate at t1, or even at a time in a fixed relation to t3 (e.g., 30 days before). ↩

- These methods are developed in further detail in “Dilution and True Economic Gain,” supra note 1. ↩

- 39,529,621 is the net total Tezos tokens created in 2019. A total of 39,648,280 tokens were created as block rewards, but a total of 118,658 tokens were burned (or destroyed) as security measures. ↩

- This figure is computed as the taxpayer’s Tezos-denominated time-weighted return. ↩

- Note that the depletion method is sensitive to the tax basis of the existing position on January 1. For simplicity, we set this basis to the market value of the taxpayer’s tokens on January 1, 2019, which provides a reasonable approximation of the situation of a typical taxpayer. See “Dilution and True Economic Gain,” supra note 1, at 1221-22. ↩