New crypto tax reporting obligations took effect on new year’s day

Here’s what you need to know and what we’re doing about it

Here’s what you need to know and what we’re doing about it

We wish you all a very happy new year! Unfortunately, the new year also brings a new law that is not only unconstitutional but also virtually impossible to comply with as a result of inaction from the IRS. It is important that every crypto user is aware of the pitfalls that have been created as this law is now in effect.

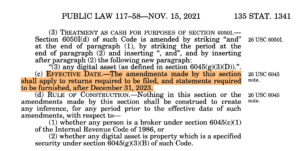

The Infrastructure Investment and Jobs Act, which passed Congress in November of 2021, included a provision amending the Tax Code to require anyone who receives $10,000 or more in cryptocurrency in the course of their trade or business to make a report to the IRS about that transaction. The report must include, among other things, the name, address, and Social Security number of the person from whom the funds were received, the amount received, and the date and nature of the transaction. If you don’t file a report within 15 days of receiving the transaction, you could be found guilty of a felony offense.

This law became effective on January 1st and all Americans are now subject to it. It is a self-executing law, meaning that there is no requirement for any additional regulatory action or implementation by a government agency for it to be enforced. Once it was passed and signed into law, it was immediately operational and enforceable on its effective date, which in this case was January 1, 2024.

In June of 2022, Coin Center filed suit against the Treasury Department challenging the constitutionality of the new law, but that case is still in the courts. Therefore, as of today, if you receive more than $10,000 in cryptocurrency in the course of your trade or business, you have to file a report within 15 days under penalty of law. Department of Justice lawyers have suggested in their court briefing that the law might not be effective before the Treasury Department issues regulations, but the IRS has never said that, and the statute itself appears by its terms to be in effect.

The problem is many will find it difficult to comply with what is supposedly a straightforward (if unconstitutional) new obligation. For example, if a miner or validator receives block rewards in excess of $10,000, whose name, address, and Social Security number do they report? If you engage in an on-chain decentralized exchange of crypto for crypto and you therefore receive $10,000 in cryptocurrency, who do you report? And by what standard should you measure whether an amount of a particular cryptocurrency is equivalent to more than $10,000? The law is silent on this matter and the IRS has not issued any guidance answering these and other questions.

More to the point, where do you even send your report? The law says that one must make a report “in such form as the Secretary [of the Treasury] may prescribe.” The Secretary requires “cash” to be reported using Form 8300, but has not explained how cryptocurrency, which is now a form of “cash” under the law, should be reported on this form.

More importantly, Form 8300 is today sent to FinCEN as well as the IRS. Unlike with physical cash transactions, FinCEN has no authority to collect reports concerning cryptocurrency transactions, so one cannot be required to send Form 8300 there. We’ve previously explained this in detail, as well as many other problems with the new law, in a short report.

It’s unclear what will happen. Will the IRS issue guidance or an updated form and submission process anytime soon? If not, people who receive qualifying amounts will find themselves in an odd position and will no doubt try to comply by notifying the IRS in any number of ways just to demonstrate good will.

It’s no doubt only a matter of time before someone either buys a table sponsorship for our annual dinner or makes a contribution of $10,000 or more to Coin Center in cryptocurrency, and then we’ll be on the hook for complying and will have to figure out a way to do so. The really tricky nature of this requirement will become clear when someone makes such a donation, but does so anonymously by simply sending us Bitcoin or Ether to our public addresses. Who could we possibly list as the sender in that case? These are all questions the Treasury Department has yet to answer.

In the meantime we just wanted to make sure you were aware of these new obligations that came into effect with the new year. We’ll continue to fight this law in court and work to figure out how compliance can be possible in the meantime.